Why are mutton prices in unprecedented territory?

Key points

- The National Mutton Indicator lifted above 900¢/kg cwt for the first time.

- Current short supply follows three years of elevated turn-off.

- Processors are competing for a much smaller pool of available sheep.

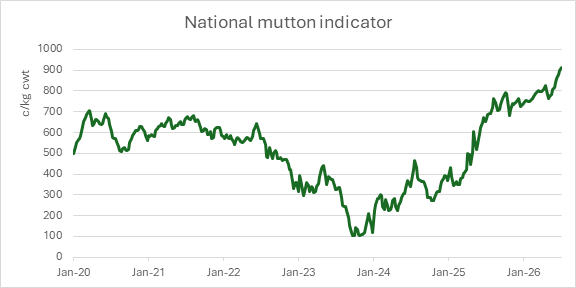

The national mutton market reached new territory this week, with the National Mutton Indicator lifting to 928¢/kg carcase weight (cwt). Mutton prices have been trading at historically high levels since the second half of 2025, but this is the first time the indicator has moved above 900¢/kg cwt, extending the sharp price recovery seen through winter.

Source: NLRS

The lift reflects a market where available sheep numbers remain limited, and buyer competition is firm. While lamb prices have also been historically strong, mutton has become the clearest example of the current supply squeeze across the sheepmeat sector. At the same time, processing capacity has expanded following several years of elevated sheep and lamb turn-off.

As a result, heavy sheep, well-finished ewes and processor-suitable lines are attracting the strongest competition. At Wagga last week, buyers paid up to $396/head for a pen of heavy ewes, highlighting the strength of demand for finished mutton.

The impact of destocking

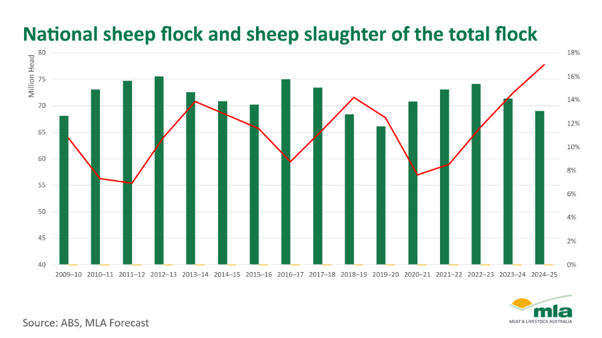

The key driver of the record price is the reduced availability of sheep. Current short supply follows three years of elevated turn-off in 2023, 2024 and 2025, largely due to destocking across southern production regions as tough seasonal conditions pressured feed availability and producer confidence.

These three years accounted for the three largest sheep supply years on record, with significant numbers moving through the system and reducing the pool of sheep now available to market. Improved seasonal conditions across parts of southern Australia have also changed producer behaviour. Where feed is now available, producers are retaining ewes, rebuilding flock numbers or holding stock rather than selling, further reducing sheep flow into saleyards and processor channels.

Processor capacity and competition

During the recent period of high throughput, processors invested in improve efficiency and expanding facilities. Since 2022, the industry has added an estimated 10 million head of sheep and lamb processing capacity through plant expansion, labour improvements and operational efficiencies.

The change is clear when looking at sheep slaughter relative to the national flock. In 2022, 6.2 million sheep (9% of the total flock) were processed from a flock of 73 million head. By FY2025, 11.7 million sheep were processed, equal to 17% of the flock and the highest slaughter pressure on the flock in recent times.

Current capacity was built around very high throughput, but supply has now tightened sharply. This has created a challenge for processors trying to secure enough sheep to maintain processing chains and has underpinned strong competition for available stock.

Current capacity was built around very high throughput, but supply has now tightened sharply. This has created a challenge for processors trying to secure enough sheep to maintain processing chains and has underpinned strong competition for available stock.

Processors have responded by reducing shifts and extending winter maintenance shutdowns. However, supply has reduced faster than the processors’ ability to adjust kill schedules. According to the NLRS slaughter report, sheep processing throughput has fallen from a recent weekly peak of 255,000 head in December 2024 to 46,000 head last week – the lowest level since July 2020.

Saleyard supply

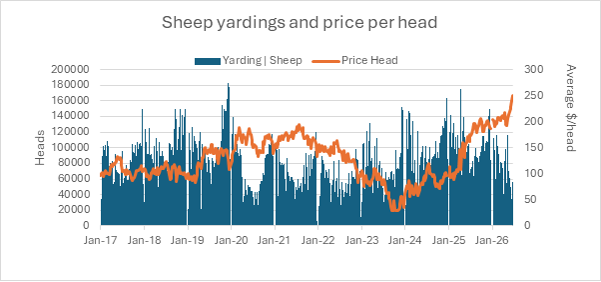

Saleyard reports show the national trend is being reinforced at key selling centres. Sheep yardings peaked in April 2025 at around 175,000 head before falling by about 80% to sit near 35,000–45,000 head in June. Wagga was a major contributor to the national result, with mutton averaging close to 980¢/kg cwt and some heavy ewe lines moving beyond 1,000¢/kg cwt.

Source: NLRS

Near-term mutton prices are likely to remain supply led. Continued ewe retention, improved feed conditions and tight saleyard numbers would keep prices supported. The main downside risks are reduced processor kill space, winter shutdowns, quality variation and price resistance from export customers.

Attribute content to: Emiliano Diaz, MLA Senior Market Information Analyst.

Information is correct at time of writing on 2 July 2026.